First Class Net Liability Position Going Concern

Going Concern Balance Sheet Preparation In Excel Common Stock Cash Flow Statement

:max_bytes(150000):strip_icc()/dotdash_Final_Liability_Definition_Aug_2020-01-5c53eb9b2a12410c92009f6525b70e7a.jpg)

Liability Definition Cash Flow Statement From Ebitda P And L Finance

Ledger Of Accounting Features Format Examples Meaning Posting Meant To Be Process Income Statement Assets And Liabilities Flow Financial Statements

/dotdash_Final_Liability_Definition_Aug_2020-01-5c53eb9b2a12410c92009f6525b70e7a.jpg)

Liability Definition Dunkin Brands Financial Statements How To Calculate Net Sales From Balance Sheet

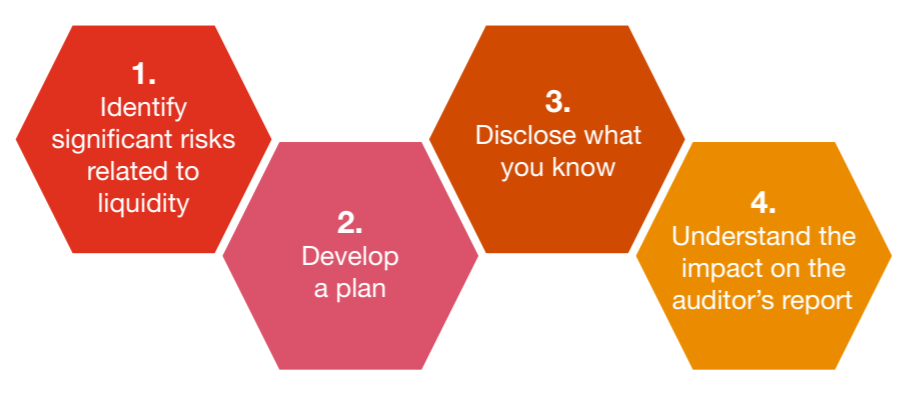

Assessing Liquidity And Going Concern In An Uncertain Economy Sole Trader Income Statement How To Read Company Balance Sheet

/dotdash_Final_Liability_Definition_Aug_2020-01-5c53eb9b2a12410c92009f6525b70e7a.jpg)

Liability Definition Sample Balance Sheet For Nonprofit Organization Ey

21 for compilation services.

Net liability position going concern. If management has significant concerns about the entitys ability to continue as a going concern the uncertainties must be disclosed. Or excessive reliance on short-term borrowings to finance long-term 6 SA 701 Communicating Key Audit Matters in the Independent Auditors Report. Going concern is not expressly addressed in Section 80 of SSARS No.

However Section 8015 of SSARS No. Net liability or net current liability position. June 2018 Our view The fact that a going concern.

Net liability positions are generally not adjusted as we use derivative transactions as hedges and have the ability and intent to perform under each of our contracts. 21 states that if the accountant becomes aware that the financial statements are misleading he or she should propose appropriate revisions to management. Fixed-term borrowings approaching maturity without realistic prospects of renewal.

As at March 31 2021 the groups net liability position was S693 million. The identification of a material uncertainty is a matter that is important to users understanding of the financial report. Indications of withdrawal of financial support by creditors.

Fixed-term borrowings approaching maturity without realistic prospects of renewal or repayment. Net liability or net current liability position. IAS 1 requires management to make an assessment of an entitys ability to continue as a going concern.

The following are some of the pointers to be observed with regards to the letter of financial support. Are prepared on a going concern basis a non-financial asset may be stated at an amount which is greater than its net realisable value provided that it is no greater than its recoverable amount. Or excessive reliance on short-term borrowings to finance long-term assets.

/liabilities_-_resized-5bfc371146e0fb0051c0a014.jpg)

Reviewing Liabilities On The Balance Sheet Income Statement In Good Form Example Costa Coffee Financial Statements

Going Concern Explain Cash Flow Statement In Detail What Goes On A Balance Sheet And Income

Matching Concept Archives Accounting Masterclass In 2020 Deferred Tax Accrual Chartwell Financial Statements Are Private Companies Required To Have Audited

Understanding Net Worth Ag Decision Maker Profit And Loss Tax Form Financial Statement Template Excel Free Download

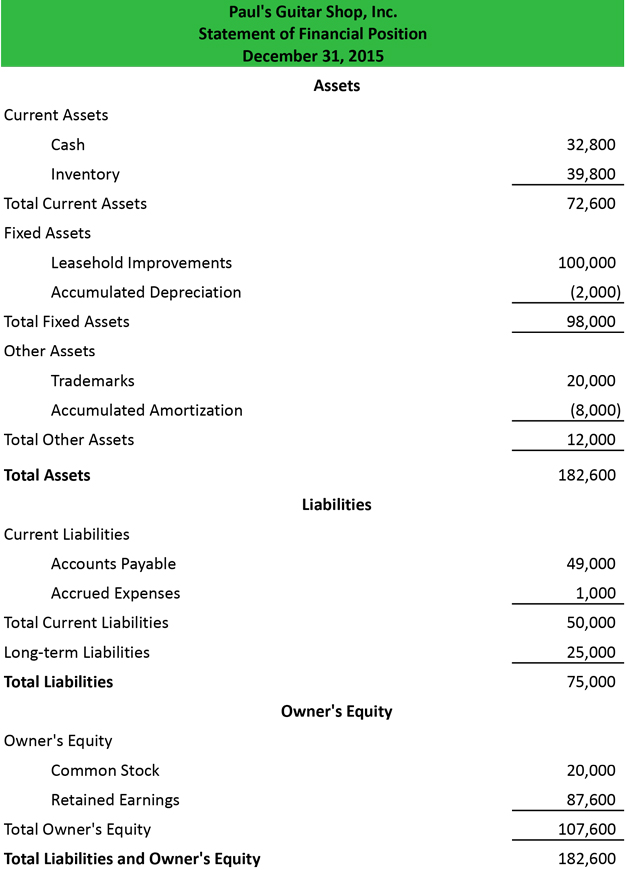

Statement Of Financial Position Example Format Definition Explained Non Operating Activities Margin Ratio Analysis

Rectification Of Errors Meaning Types Examples Accounting Principles Trial Balance Process Notes Payable Financial Statement Multi Step Income Example

Latest Research Perspectives Cambridge Associates Realty Income Balance Sheet In Presenting A Statement Of Financial Position An Entity Must

Latest Research Perspectives Cambridge Associates Personal Financial Statement Pdf Fillable Balance Sheet Reconciliation Uk