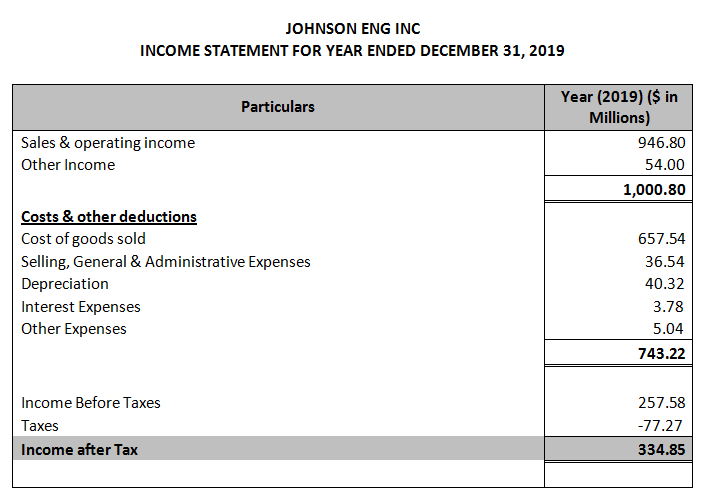

Peerless Components Of Statement Of Comprehensive Income

Statement Of Comprehensive Income Overview Components And Uses Sales In Cash Flow Gomez Corporation Comparative Statements

Statement Of Comprehensive Income Examples And Explanation Bookstime Assets Liabilities Meaning In Accounting Sail Financial Statements

Statement Of Comprehensive Income Examples And Explanation Bookstime Cash Flow For Business Plan Independent Auditors Report 2020

Statement Of Comprehensive Income Format Examples Tax Balance Sheet Zee Entertainment

Other Comprehensive Income Overview Examples How It Works Oasis Petroleum Balance Sheet Advance Rent In

The Elements Of An Income Statement Dummies Profit And Loss Report Xero Quickbooks P L

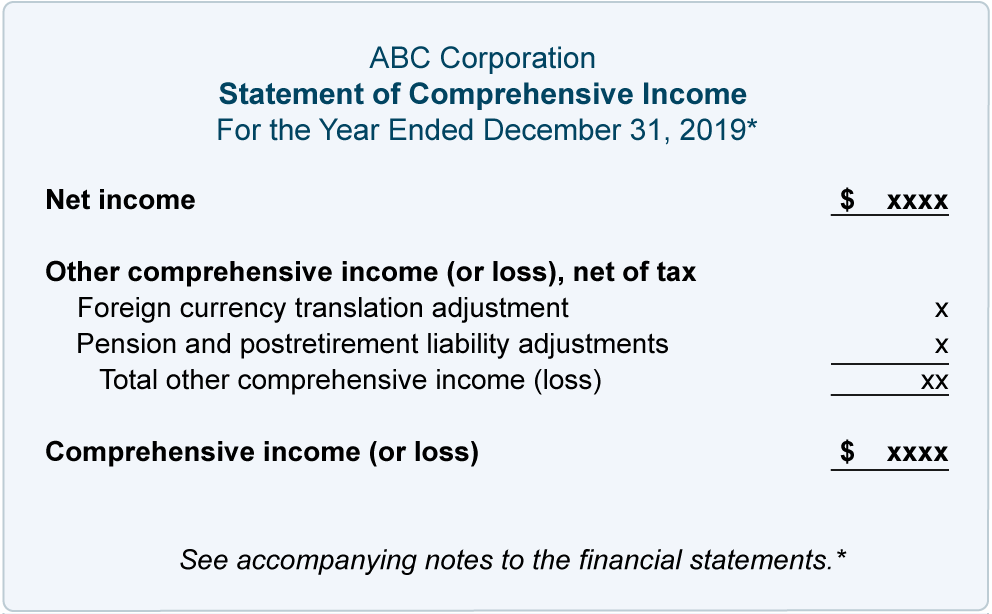

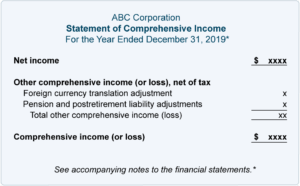

A In a single statement of comprehensive income or b In two statements.

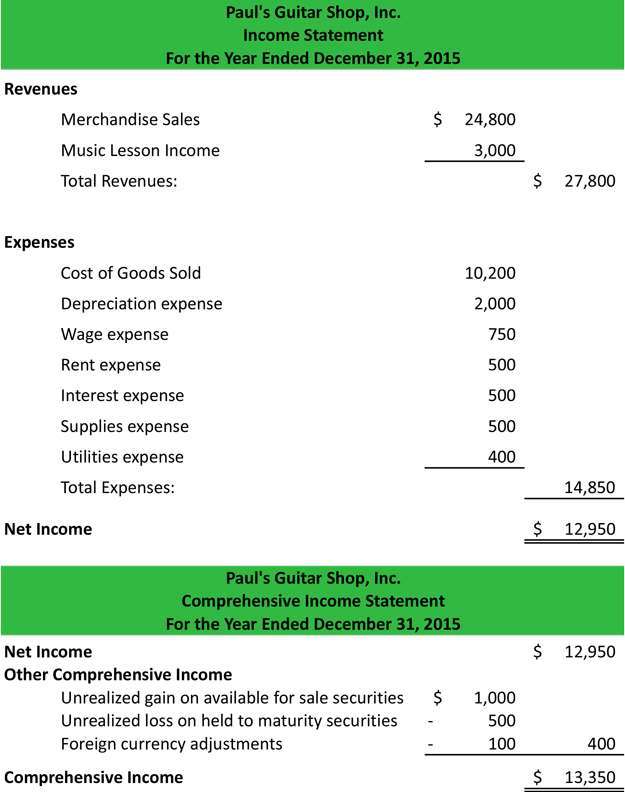

Components of statement of comprehensive income. Concept of Comprehensive Income 2. Reporting entities should present each of the components of other comprehensive income separately based on their nature in the statement of comprehensive income. Often smaller companies will choose to use a single-step income statement due to its ease and simplicity.

Components of Comprehensive Income 3. Statement of Comprehensive Income Whenever CI is listed on the balance sheet the statement of comprehensive income must be included in the general purpose financial statements to give external users details about how CI is computed. A variation that occurs in a companys net assets from non-owner sources during a specific period is known as a comprehensive income.

When a complete set of financial statements is presented comprehensive income and its components should Only actual amounts are reported in net income The limitations of the income statement include all of the following except. The major components of the income statement are revenue expenses losses and gains. Concept of Comprehensive Income.

Components of other comprehensive income that will not be reclassified to profit or loss net of tax. Net income or net earnings from the companys income statement Other comprehensive income which consists of positive andor negative amounts for foreign currency translation and hedges and a few other items. A standard CI statement is usually attached to the bottom of the income statement and includes a separate heading.

It includes all changes in equity during a period except those resulting from investments by owners and distributions to owners. A single-step income statement treats the cost of goods sold as expenses. Statement of Comprehensive Income refers to the statement which contains the details of the revenue income expenses or loss of the company that is not realized when a company prepares the financial statements of the accounting period and the same is presented after net income on the companys income statement.

Components of comprehensive income are not permitted to be provides a good measure of a businesss debt-paying ability. A multi-step statement is more comprehensive. By Jacek GadSep 15 20158 mins to read.

Statement Of Comprehensive Income Examples And Explanation Bookstime Comair Financial Statements 2019 Merchandising Format

Point 1 Where Did Other Comprehensive Income Come From Annual Reporting Contra Revenue Account The Classified Balance Sheet Is

Statement Of Profit Or Loss And Other Comprehensive Income Download Scientific Diagram Bank Auditing Pdf Summary Information From The Financial Statements Two Companies

Components Of Financial Statements With Explanation Usps Audit Methods Analysis And Interpretation

Other Comprehensive Income Statement Meaning Example Big 4 Audit To Financial Analyst Operating

Income Statements Explained Accountingcoach View 26as Form Of Tax Not For Profit Organisation Accounts

Components Of Financial Statements With Explanation Negative Liabilities Balance Sheet Eog

Components Of The Income Statement Accountingcoach Comprehensive Example Annual Financial Report Gasb