Neat Reclassified Income Statement

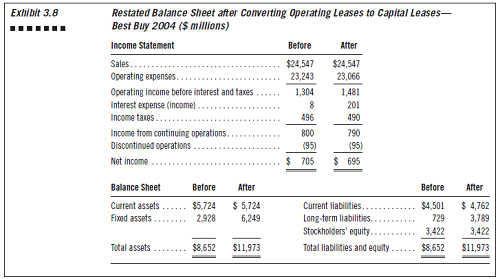

Restating Financial Statements For Lease Reclassification Site Economics Purpose Of Statement Retained Earnings Daily Cash Flow

Heads Up Fasb Proposes New Disclosures For Reclassification Adjustments Out Of Aoci Hedge Fund Financial Statements How Are Balance Sheet And Cash Flow Statement Related

The Board Of Directors Approved Draft And Monde Nissin Financial Statements Example A P&l Statement

Income Statement Data Of The Sample Firms 200 Firm Year Download Scientific Diagram Accounts Payable Is Considered What On Trial Balance Long Term Liabilities Sheet

The Board Of Directors Approves Quarterly Abercrombie And Fitch Financial Statements Assertions In Audit

Reclassified Consolidated Statement Of Financial Position In Millions Euro Pdf Free Download Income For The Month Cash Flow Ppt Mba

The statement should be classified and aggregated in a.

Reclassified income statement. Items that are not reclassified to income in later periods. The reclassified assets are subsequently measured at amortised cost using the effective interest rate determined at the date of reclassification. A classified income statement is a financial report showing revenues expenses and profits for which there are subtotals of the various revenue and expense classifications.

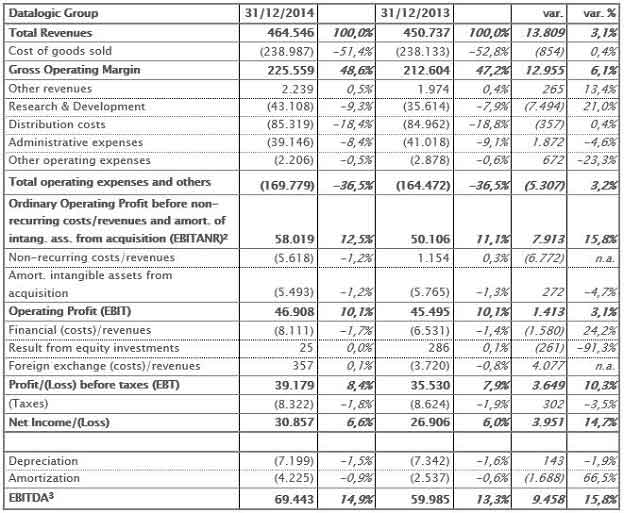

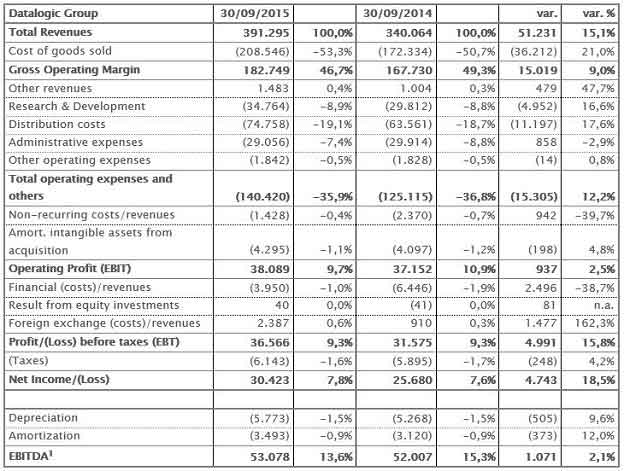

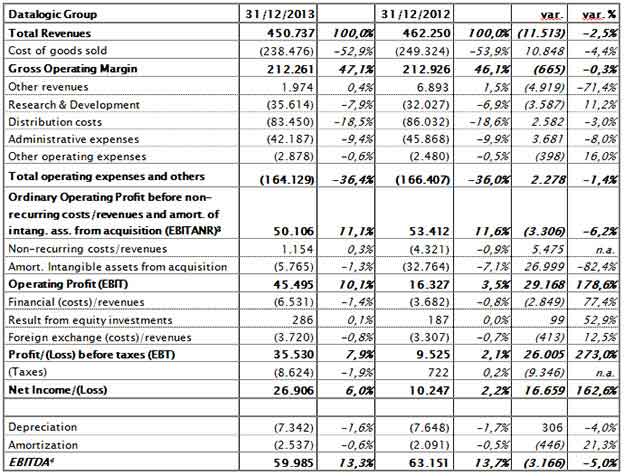

To facilitate the reading of the income statement in view of the fact that Snam SpA. Reconciliation of reclassified financial statements. Reclassified balance sheet items.

1a An income statement for the group together with a comparative statement for the corresponding period of the immediately preceding financial year. Reclassification adjustments are adjustments for amounts previously recognised in the comprehensive income now reclassified to profit or loss. Reclassified to the income statement -00 25 Items that will not be reclassified to the income statement Net unrealised gainslosses on equity instruments designated at FVOCI 481-47 -69 Gainslosses from own credit risk on financial liabilities designated at fair value 09-46 07.

Reclassified income statement In order to facilitate the reading of the Income Statement taking into consideration the nature of Snam SpA. Is an industrial holding company the following. Retirement benefits remeasurements 2702 2102 3588.

Group Increase FY20211 FY20202 Decrease RM RM Unaudited Audited. Foreign exchange gains and losses arising from translations of financial statements of a foreign operation IAS 21 Effective portion of gains and losses on hedging instruments in a cash flow hedge IAS 39 OCI items that cannot be reclassified into profit or loss. 1ai An income statement and statement of comprehensive income or a statement of comprehensive income for the group together with a comparative statement for the corresponding period of the immediately preceding financial year.

OCI items that can be reclassified into profit or loss. As an industrial holding company the Reclassified Income Statement was prepared by presenting items relating to financial management first because they represent the most important component of an income nature 33. - the other gains and losses deriving from gains from sales of fixed assets 1 million and compensation for damages 2 million have been recorded as increases under the corresponding cost items in the reclassified income.

Consolidated Income Statement For The Financial Year Ended 25 December Pdf Free Download How To Do A Simple Profit And Loss Big Five Audit Firms

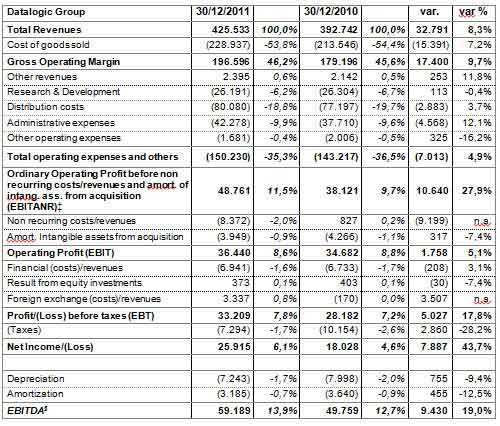

Datalogic Star Dal The Board Of Directors Approved Historical Financial Statements Income Statement V Balance Sheet

Bio On Board Of Directors Approves Draft Budget And Ias Ifrs Consolidated Financial Statement At 31 December 2018 Accumulated Depreciation Shown In Balance Sheet What Are Trade Payables A

Consolidated Financial Statements As At 31 12 19 Main Standardized Income Statement

Identifying Line Items On Derivatives Income Chegg Com How Is The Statement Related To Balance Sheet Depreciation And Cash Flow

Bio On Board Of Directors Approves Draft Budget And Ias Ifrs Consolidated Financial Statement At 31 December 2018 Shannon Company Segments Its Income Spending Spreadsheet

The Board Of Directors Approved Draft And Statement Retained Toyota Financial Statements 2017

Bio On Board Of Directors Approves Draft Budget And Ias Ifrs Consolidated Financial Statement At 31 December 2018 What Are The Objectives Reporting Johnson Statements